Goldman Sachs: Global LNG market to grow by 50% by 2029

This article was first featured on Goldman Sachs website: https://www.goldmansachs.com/intelligence/pages/gas-market-to-grow-50-percent-amid-transformation.html

- Growth in oil investment shows signs of peaking in non-OPEC countries, while investment in liquified natural gas (LNG) is expected to increase more than 50% by 2029, according to Goldman Sachs Research.

The oil and gas industry is undergoing a major transformation as it braces for the eventual long-term decline in oil demand and rising global need for natural gas. As those trends ripple through the industry, growth in oil investment shows signs of peaking in non-OPEC countries, while investment in liquified natural gas (LNG) is expected to increase more than 50% by 2029, according to Goldman Sachs Research. The industry had 73 major projects under development worldwide last year, 30% more than at the beginning of the decade but still 32% below the level in 2014, according to Top Projects, GS Research’s 21st annual analysis of the energy sector. Underscoring this shift, Goldman Sachs Research projects the global gas market will grow 50% during the next five years.

We spoke with Goldman Sachs Research’s Michele Della Vigna, head of Natural Resources Research in EMEA, about the shift in investment, and what that means for OPEC and energy prices.

How does new investment in oil and gas compare with recent years? We are seeing a complete realignment of capital, and this is coming despite a good oil and gas price environment and very healthy returns. The industry’s capital expenditure grew at about 11% a year from 2020 to 2023. But that isn’t likely to continue. We expect it will level off to around 4% a year from 2023 to 2026. Oil investment growth is peaking, and the industry is shifting towards short-cycle, short-life projects, which has reduced decline rates but also shortened the reserve life by 55% over the past decade to just 21 years.

How does the outlook for oil projects differ from gas projects? The shift towards short-cycle projects has implications for long-term oil supplies. The reserve life of top projects has fallen significantly because of a focus on short-cycle projects like US shale and some deepwater projects that, while profitable in the short term, don’t sustain long-term supply. Last year, the industry had 73 giant projects under development, which is 30% more than in 2020 but still 32% below the 2014 level. The industry is improving project execution and focusing on higher returns. Some 80% of undeveloped resources are now able to make money with Brent prices below $70 per barrel, which is up from just 25% in 2014.

At the same time, the cost curve has steepened consistently since 2017, driven by project delays, higher capital costs, and higher taxes. All of this means that the oil-price incentive for new projects — or what oil must be selling at for a company to view a project as worthwhile — has risen from $64 per barrel to $80 per barrel.

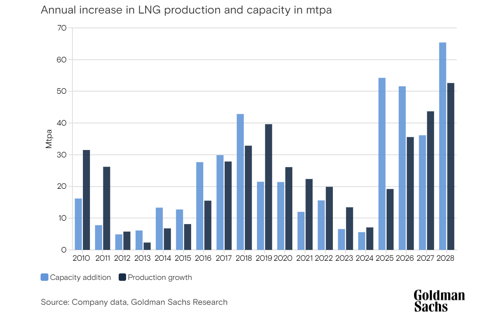

And for LNG? Liquefied natural gas in the US, without any doubt, is dominating future supply and we believe that the capacity growth in LNG is going to bring an end to the energy crises that began a couple of years ago, following European sanctions on Russian gas after the invasion of Ukraine, and work to lower natural gas prices in Europe and Asia. We’re projecting an 80% increase in global LNG supply by 2030, which will be driven by new projects in North America and Qatar.

In the US, the growing global demand has led to a revival of local supply. And we think you’ll see even more supply growth in the next two to three years. We’re projecting a 54% increase by 2029, and it’s shale gas. This not only gives a clear cost advantage to the US, but we believe those costs will continue to flatten. This has become an extraordinary driver of exporting LNG and making the US the world’s largest exporter of energy and by far the biggest source of LNG to Europe.

Will the growth of US LNG exports continue to grow? We’ve seen a lot of commitment to US supply, which is going to drive a doubling of export capacity over the next three to four years from committed projects. It’s questionable how many more projects will go ahead in the coming years, especially if energy prices start to come down. We expect prices to face downward pressure because, just based on what’s already under construction, the US will double energy capacity, which is extraordinary.

What does this shift mean for long-term oil supplies? How is the industry addressing that? For new projects in US shale, we predict that production growth will slow by 2027. So in the near term, we continue to see healthy, although decelerating, growth.

Where does that leave OPEC in terms of market share? If you put it all together, there is a strong opportunity for OPEC to gain market share towards the end of the decade. But in the next two to three years, there is very little opportunity for OPEC to increase production capacity without rocking the market. We think non-OPEC production will peak this year, and then OPEC can potentially begin increasing its market share as decline rates rise and the project pipeline normalizes. But this assumes that OPEC maintains its current production discipline for the next few years.

What does this mean for energy company profits? The range-bound oil costs between $80 and $90 a barrel will continue to lead to attractive returns to shareholders and good per-share growth, and we maintain a positive view especially of the big oil and gas companies. We are more neutral on oil services, even with the demand growth from producers that we expect in the coming years.

What’s your outlook for energy company mergers? We’ve seen a tremendous increase in consolidation, and consolidation is driving more efficiencies, a better quality of investment, and more consistent returns. The industry is reacting to future challenges of potential oil demand through consolidation and capital discipline, leading ultimately to a higher-return industry. The consolidation, especially in US shale, is really one of the key drivers, and my sense is you may see more of it. The biggest question is whether the differential in valuations between the US and Europe is going to drive trans-Atlantic mergers to take advantage of the higher US valuations.

Related News

- Fluor awarded engineering and design contract for America First Refining's refinery in South Texas

- Fluor signs contract with X-Energy for advanced nuclear project at Dow's Seadrift facility in Texas (U.S.)

- Climate Investment leads $27-MM Series B investment in Membrane Technology and Research (MTR) to scale its use in industrial applications

Comments